Mfr of crushing and grinding parts for mining, cement, power

AIA Engineering

Founded in 1991

Headquartered in Ahmedabad, Gujarat

Sectors - Gold, Industrials, Infra, Power

Listed in -2005

NSE Ticker - AIAENG

BSE Ticker - 532683

A clean laser focused Company

The simplest but most relevant analysis you will find on the Company. Read slowly, think carefully & you might agree !.... Do comment at the end for any clarification/ views.

Summary

Company deserves a serious look by long term investors. Can be a decent compounder.

Sector Interest

😐 Cyclical. Dependent on sectors like mining, cement, power.

Management

😇 Highly focused management who seems to be following a clear line of strategy.

Financials

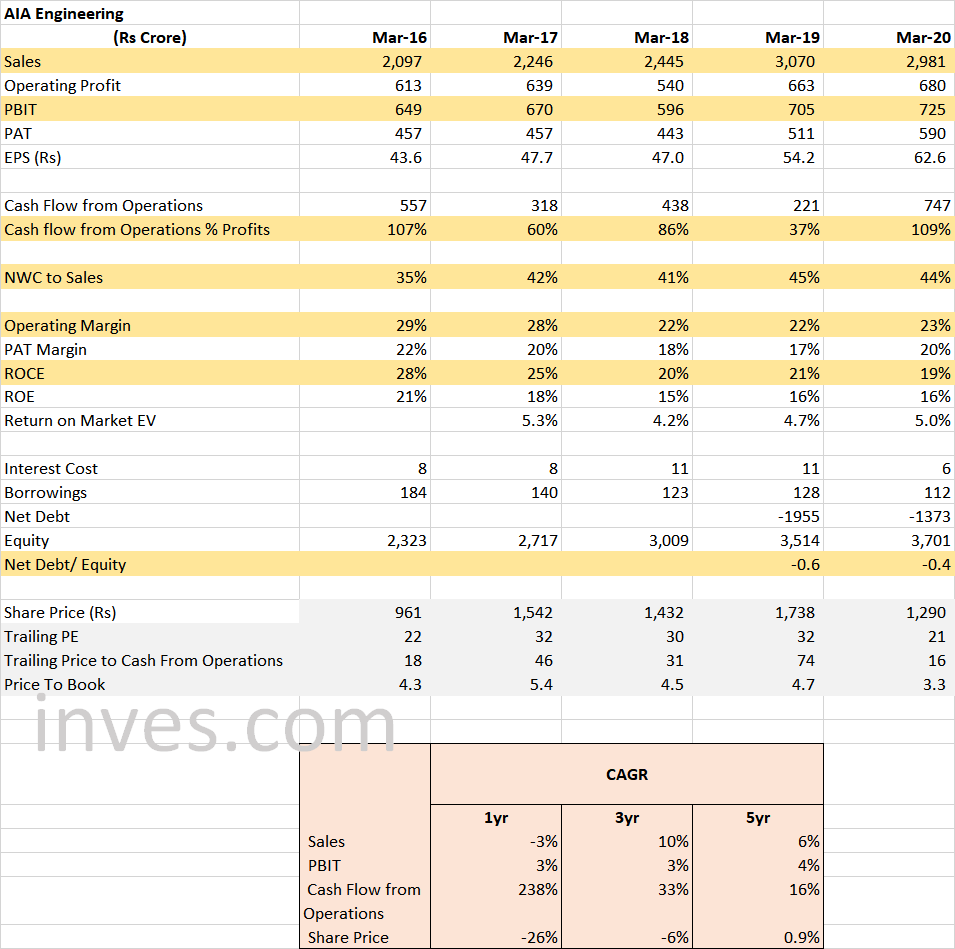

😊 Solid margins, debt free Company. However, being cyclical, sales growth fluctuates.

Valuations

🙂 ok types. On the lower side vis-a-vis historical levels but not at a steep discount.

Technicals

🙂 Consolidating since 2015 and can provide significant returns in case of a breakout

Investor Interest

😇 Significant interest from institutions who currently hold 38%. Retail holding is less than 3% !

SWOT

Strengths

- Company’s products being of consumable (wear and tear) nature, get repetitive demand from the customers.

- Well diversified – AIA sells across 125 countries to more than 500 customers mitigating country/ customer specific risk.

- Focused reliable management – listen to some of their conference calls and read annual reports to get an idea on the quality of management. (Do refer to one of my previous articles of what I generally look in any management – Management commentaries and what I make of them)

- Solid margins – PAT margin of about 20% – I don’t know many Companies that have those kind of margins. (my reasoning for high margins is provided in the financials section)

- Debt free Company with significant liquidity in hand. Current liquidity is estimated at Rs 1,600 cr which is equivalent to 10% of the current market cap. This is only expected to add up as we move forward that in turn will provide sufficient resources for organic/ inorganic expansions and/ or rewards to the shareholders.

Weaknesses

- Cyclical nature of sectors that the Company supplies it’s products to.

- One may also be prompted to call management over cautious and averse to get out of it’s comfort zone. Debt is negligible, liquidity is significant and still you will not hear management sounding aggressive. Different investors look at this differently and that does reflect on it’s share price movements.

Threats

- New business development has slowed down significantly due to Covid led disruptions especially on the international travel. Company’s products require physical discussions.

- Global recession – a prolonged slowdown will surely impact Company’s fortunes both actually and sentimentally. Result – the impact on it’s share price can be higher than traditional recession proof sectors.

- Succession Planning – Company’s designated MD continues to be it’s founding promoter who is approaching 70 yrs. Both his daughters are on the board but historically had very different interests. Though most of the day to day operations seem to be delegated and run by the professional management, actual procedural succession still remains a question mark. (This is true for many-2 Indian Companies)

Opportunities

- Mining is the main focus segment of the Company – 65-70% of its revenues comes from this sector wherein it mainly supplies niche ‘chrome’ grinding media products. Worldwide grinding media products required in mining is estimated at 2.5 mn tonnes annually of which 20% is chrome based and balance 80% traditional forge based. Chrome offers significant operational and durability advantages over forged. To put it in perspective, out of 2.5 mn tonnes in FY 20, AIA supplied just 0.18 mn tonnes i.e., 7%. This is where Company is putting most of its efforts both in terms of developing new customers as well as converting forge based requirements to chrome based. Besides, Company is also working to increase its wallet share with existing customers by offering related products e.g., mill liners.

- Company should also be a direct beneficiary of widely expected infrastructural led economic revival efforts by governments across countries and hence increased demand from the cement and power sectors.

Management Quality

- AIA was founded by Mr Bhadresh Shah, the current MD of the Company. He is a metallurgy engineer from IIT Kanpur.

- He originally started with a small foundry in 1978 and then incorporated AIA in 1991.

- For all practical purposes, one can call AIA to be an original promoter driven Company supported by hand picked well regarded professionals.

- When I looked into the details of the Board, operational management, ESOP patterns, remuneration etc – I again got a feeling of AIA being contented and cautious.

- Succession planning – as mentioned before remains a question mark.

Financials

Auditors - M/S BSR & Co LLP

Bankers - SBI, Axis, Citi, HSBC, IDBI

Credit Rating -

Crisil AA+ (Stable), A1+

To a patient investor AIA should reward well

- Being dependent on the cyclicals, sales growth moves in pockets. 65-70% sales come from mining sector (gold, platinum, iron ore and copper ores) and balance from others including cement and thermal power. 75% of Company’s sales is from exports and balance 25% from domestic.

- Margins are solid. In my view, Company enjoys good margins as it falls into the category of essential but low cost items – so more than price, customers should be bothered about quality and efficiencies and that’s where AIA seems to be traditionally focused upon. (Just for calculation: 500+ customers and Rs 3,000 crore of revenue means on an average Rs 6 crore per customer)

- Raw material – 65% of input material is sourced from scrap which in turn is sourced from the ship breaking industry. Though prices fluctuate, it’s mostly a pass through, albeit with some lag.

- Return ratios though have declined over the years, continue to be reasonably attractive.

- Company’s current installed capacity is 3,90,000 TPA and the current plan is to increase it by 50,000 TPA each in current year and next year. On pre-Covid basis the capacity utilization would have stood at about 70% and post Covid currently at around 55-60%. Given these numbers, there is sufficient headroom to manage growth in foreseeable future. Besides, Company has further available liquidity of Rs 1,600 crore which will further increase as we move forward. A 50,000 TPA expansion recently costed Company Rs 250 crore. These numbers are extremely comfortable from future expansions perspective.

- Valuations are lower than historical levels but are not very attractive. (Note: March 20 valuations are calculated at Rs 1,290/ share. Accordingly, please adjust the same as per the current market price)

Important Links

Technicals

- Stock has done almost nothing over the last 5 years and in the March meltdown also touched it’s 2015 breakout levels.

- Currently, the stock continues to consolidate and nearing it’s breakout levels.

- In case of a breakout, one can expect significant returns over a short period.

- Till then, price movement can be expected in between Rs 1500-1800.

INVES4 MODEL PORTFOLIO

An actively managed portfolio - cross between fundamental and technical analysis

Disclaimer: The information presented above is no advice/ recommendation. Please do your own independent research before taking any investment related decision.